This article originally appeared on April 22, 2020 at www.woodmac.com.

It’s been four years since the Paris Agreement was negotiated, yet global emissions have continued to rise each year. To achieve the agreed 2°C goal, global emissions need to peak as soon as possible and trend towards net-zero by 2070.

Major cities around the world have seen significant falls in greenhouse gasses in recent weeks as the coronavirus affects work, travel and industrial activity. As a consequence, many countries will unintentionally experience lower emissions this year.

After the global financial crisis in 2009, emissions rapidly rebounded with stimulus spending that boosted fossil fuel use. So how governments stimulate their economies once this pandemic eases will significantly impact future emissions. Sustained investment in renewable technologies is required now to reduce emissions over the longer term.

Roughly a third of today's greenhouse gas emissions come from the burning of fuel for road, air, rail and marine transport. This is the largest sector for emissions, more than even power, but battery technology has made both these sectors' emissions easier to abate. In contrast to industrial sectors like steel and cement, cost-competitive low-carbon technologies already exist for transport and power, and both rely upon batteries.

Under the Wood Mackenzie 2°C pathway , emissions from the transport sector must halve before 2040. To maintain the same level of transport connectivity, 900 million vehicles with a plug would need to be on the road by then, making up over half of the global fleet. But in 2019, just 10 million vehicles – 2% of the fleet – were electric. At its peak the EV industry would need to manufacture 70 million a year to replace internal combustion engine counterparts.

Likewise, wind and solar must generate the majority of electricity output by 2040. But generation at this level will only be enabled by having batteries in place to store the power for when it is required.

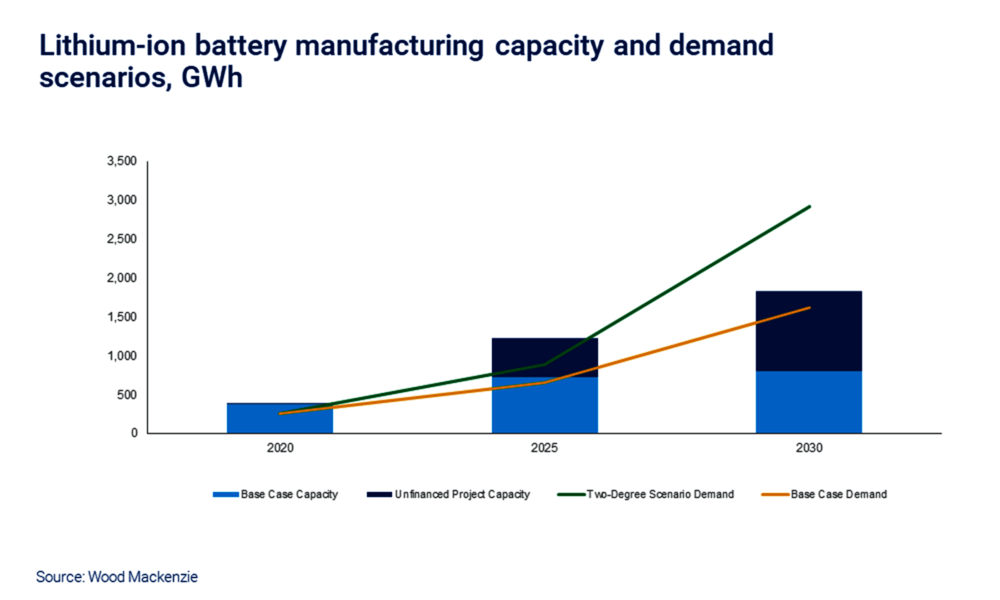

To provide these industries with the batteries required, manufacturing capacity needs to grow 10-fold, to just under 3,000 GWh in 2030. If all the currently planned manufacturing plants are constructed on schedule – a big if – the industry will still only grow to around 1,800 GWh by 2030. But right now, less than half this capacity has been financed. And that’s where some fundamental issues emerge.

The current rate of development of the battery sector and raw materials is not enough to support emissions reductions in line with the 2°C target. Indeed, based on today's investment and technologies, Wood Mackenzie's outlook for energy markets forecasts emissions leading to 3°C warming by the end of this century.

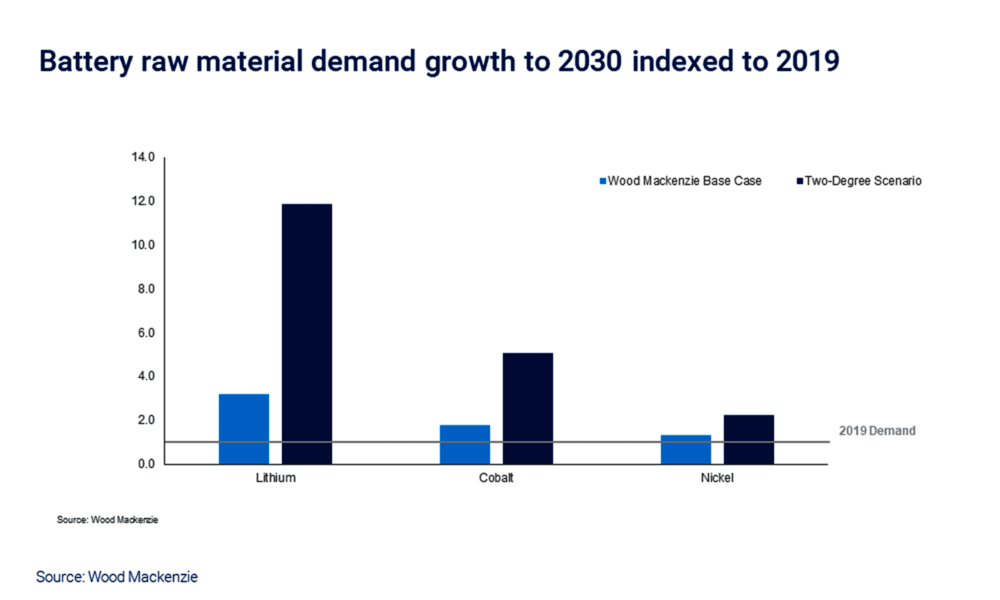

To limit warming to 2°C, faster growth of battery manufacturing is the primary requirement, but the scarcity of raw materials drives the need for diversification of storage technologies as well. This includes more fuel cells to complement now-dominant lithium-ion batteries. Within lithium-ion itself, nickel-intensive chemistries must be supplemented by lower energy density cathode types like Tesla has picked for one of its Chinese models.

In short, sufficient decarbonisation of the transport and power sectors needs long-sighted investors to support the accelerated development of new capacity – and emerging technologies – across the battery value chain.

Author: James Whiteside, Research Director, Global Head of Multi-Commodity Research | Wood Mackenzie

Image: Pixabay |

www.pixabay.com

The ees International Magazine is specialized on the future-oriented market of electrical energy storage systems, not only from a technological-, but also a financial and application-oriented point-of-view. In cooperation with ees Global, the ees International Magazine informs the energy industry about current progress and the latest market innovations.